All MLOs have to complete real estate continuing education, but the best don't stop there. Our industry is ever-changing, and the most successful lenders are the ones who never stop learning.

That’s why we’ve put together this collection of deep-dive resources just for you. These resources go beyond what's covered in our 8-Hour SAFE Comprehensive: Balancing AI and the Human Element (2025) and 7-Hour SAFE Core: MLO Essentials (2025) CE courses, giving you deeper insights, fresh perspectives, and actionable strategies to apply in your day-to-day business. So dive into these expert-approved reads and keep pushing your business forward.

Fair Lending and Credit Laws (ECOA, FCRA, TILA)

Fair Lending 2024: Top 7 Takeaways

This blog covers hot-button Equal Credit Opportunity Act (ECOA) issues – from why fancy algorithms won’t save you from discrimination rules to real-world case studies (like a bank that preyed on minority borrowers with predatory ARMs and got sued under ECOA). If you’re curious about what regulators are watching (immigration status in lending decisions, marketing mishaps, etc.), this quick-read list gives practical pointers and cautionary tales to keep you out of trouble.

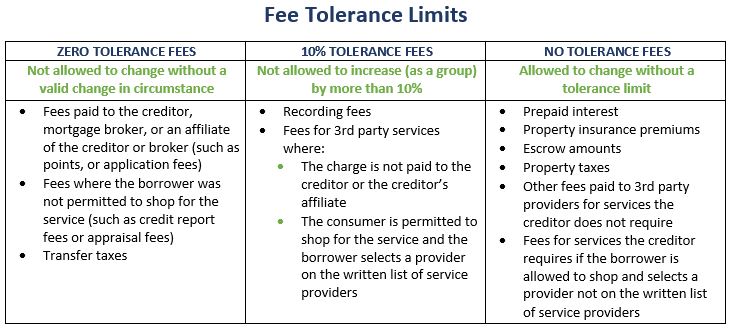

Eight Common TILA-RESPA Errors

Think you’ve mastered the Truth in Lending Act (TILA) disclosures? This article might change your mind. It walks through 8 frequent mistakes lenders still make with Loan Estimates and Closing Disclosures, even years after TRID implementation. Whether it's missing change-of-circumstance documentation or mishandling fee tolerances, it’s a practical checklist of “uh-oh” moments to avoid. The tone is straightforward and actionable – perfect if you want to prevent costly TILA slip-ups before they happen.

Ethics and Servicemember Protections

Mortgage Fraud Cases – “The Good, Bad and Ethical”

If you enjoy a little true-crime flavor, this roundup of recent mortgage fraud cases will hook you. It spotlights several eye-popping schemes – like developers and even loan officers caught in multi-million dollar frauds – and asks whether these harsh sentences are a sign of more to come. It’s a candid look at what happens when ethics go out the window. Reading these cautionary tales is not just fascinating – it’s a stark reminder of why we have those ethics rules in the first place (and the consequences of breaking them!).

Deceptive VA Loan Advertising Crackdown

Imagine being banned from the mortgage industry for life – that’s what happened to one lender in this wild enforcement story. This article details how, within the last few years, a company repeatedly misled veterans with fake government affiliations and “too good to be true” loan offers, even after being warned. It’s a dramatic read that underscores the importance of honest marketing, especially for VA loans. If you work with servicemembers, you’ll want to see how bad actors got caught so you can avoid a similar fate.

Servicemembers Civil Relief Act (SCRA) Overview

Serving those who serve our country comes with special responsibilities, and this guide lays them out in plain English. It covers SCRA protections like the 6% interest rate cap during active duty and the rules preventing foreclosure on deployed servicemembers. Written in a friendly tone by a VA loan expert, it translates the legalese into what it means for lenders and military borrowers. It’s a feel-good refresher on how we can help our military clients – and stay above board – by knowing their rights.

Anti-Money Laundering (BSA/AML)

Cracking Down on Money Laundering in Real Estate

Dirty money has a way of sneaking into real estate, but new rules are coming to stop it. This article explains FinCEN’s latest moves to unmask secret buyers and require reporting on all-cash deals. It cites an eye-opening stat – at least $2.3 billion was laundered through U.S. real estate in just a few years – illustrating why regulators are cracking down. The piece is an easy read on a serious topic, listing red flags and what the changes mean. If you want to see how anti-money laundering laws are evolving, give this a read.

Non-Traditional Mortgage Products (ARMs & HELOCs)

Adjustable-Rate Mortgages Are Back

Is it 2005 again? Not quite, but ARMs are making a comeback. This insightful article dives into how adjustable-rate mortgages jumped from just 4% of originations to 15.5% by mid-2024 as buyers hunt for affordability. It contrasts today’s safer, regulated ARMs with the wild “teaser rate” days that fueled the 2008 crash. Written in a story-driven style, it helps you understand why more borrowers are choosing ARMs now and what could happen if rates change. It’s a timely read that will make you the go-to expert when a client asks, “Should I consider an ARM?”

HELOCs in Vogue Again – Experian 2025 Study

Home equity lines of credit are suddenly cool again, and this study shows it. Experian reveals that HELOC balances shot up 7.2% in 2024 after years of decline. In fact, since 2023 there’s been roughly one new HELOC for every two new mortgages – wow! The article explains why (hint: homeowners love their low first-mortgage rates and aren’t refinancing). It’s full of neat stats and charts, but explained in plain language. If you want to understand the HELOC revival – who’s using them, how big the balances are, and why they’re “in vogue” – this piece is worth your time.

Freddie Mac Mortgage Programs

Freddie Mac Home Possible® – 3% Down, Big Benefits

This guide breaks down Home Possible, Freddie Mac’s flagship low-down-payment program, in a super approachable way. It feels like having a friendly colleague explain the perks: only 3% down needed, easier credit terms, and lower costs for borrowers. It even notes that many middle-income families can qualify, not just first-timers. If you’re looking for a refresher or a tool to help explain Home Possible to clients, this article has you covered – it’s upbeat, factual, and makes a great case for why Home Possible can be a game-changer for buyers.

HeritageOne℠ – New Native American Lending Program

Curious about Freddie Mac’s innovative program for Native American borrowers? This news piece gives a quick overview of HeritageOne, which offers affordable conventional loans on tribal lands. It highlights why this matters – historically, access to financing on reservations has been tough. There are quotes from Native community leaders celebrating the potential to build generational wealth. The tone is optimistic and informative. In a few paragraphs, you’ll understand how HeritageOne works and why it’s “breaking new ground” in serving an underserved community.

Refi Possible® – Refinance Relief for Low-Income Borrowers

When rates were low, some homeowners felt left out because they didn’t qualify to refinance. Enter Refi Possible, which this article calls an “accessible refinancing” option. In a reader-friendly way, it outlines the generous guidelines – for instance, debt-to-income ratios up to 65% are allowed! Even with little home equity or a modest income, borrowers can snag a lower rate and even get an appraisal credit. The piece is encouraging and easy to digest, so you can quickly grasp how Refi Possible (and Fannie’s similar RefiNow) might help your clients save money. It’s basically a cheat sheet to a program every MLO should know about.

Artificial Intelligence in Mortgage Lending

AI Bias in Mortgage Decisions

This eye-opening article explores a study where researchers tested AI underwriting – and the results will make your jaw drop. The AI models (like GPT-4) ended up recommending higher rates for Black applicants and approving white applicants more often even with identical profiles. It’s a stark reminder that without careful oversight, algorithms can pick up human biases. The article is a thought-provoking read, breaking down in simple terms how “black box” AI decisions could unintentionally violate fair lending. If you’re intrigued (or concerned) about the rise of AI in lending, this piece shows why the human element is still so important in our industry.

ChatGPT: The LO’s New Best Friend

Can an AI be your personal assistant? This fun article shows how ChatGPT is doing just that for loan officers. It’s basically a highlight reel of cool tricks – writing client emails and social posts, creating video scripts, and even drafting home listing descriptions in seconds. The tone is enthusiastic and practical, coming from an industry vet who literally wrote the book on ChatGPT for mortgage folks. You’ll learn how LOs are saving hours on marketing and admin tasks by letting AI handle the grunt work (all at zero cost!). If you’ve been curious about using AI to boost your productivity (and impress real estate agents with speedy service), this read will get your wheels turning.